Then we calculate the Present Value for each of the years – which is equal to free cash flow multiplied by the discount factor for each year. Since neither terminal value calculation is perfect, investors can benefit by doing a DCF analysis using both terminal value calculations and then using an average of the two values for a final estimate of NPV. A company’s equity value can only realistically fall to zero at a minimum and any remaining liabilities would be sorted out in a bankruptcy proceeding. It’s probably best for investors to rely on other fundamental tools outside of terminal valuation when they come across a firm with negative net earnings relative to its cost of capital.

Advantages and Disadvantages of Discounted Cash Flow Analysis

- The exit multiple approach applies a valuation multiple to a metric of the company to estimate its terminal value.

- For example, start-up businesses have high growth expectations and should incorporate a longer projection period as compared to a mature business.

- Careful use of the value driver model may help to avoid some of the issues of a growing perpetuity.

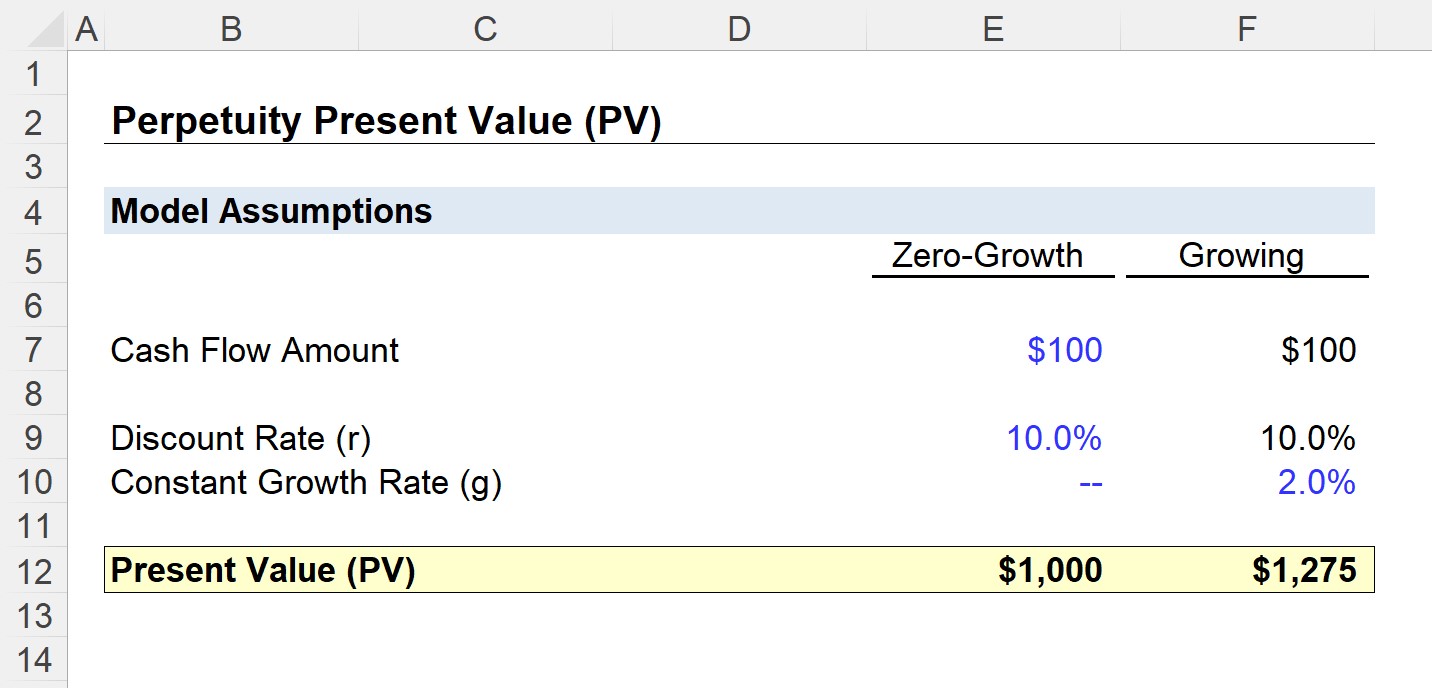

- The British-issued bonds known as consols were an example of a financial instrument with perpetual cash flows.

The problem with this approach is that you need quick access to data for comparable companies, which may be tricky without Capital IQ, FactSet, or similar services. The Cost of Preferred Stock is similar because Preferred Stock works similarly to Debt, but Preferred Stock Dividends are not tax-deductible, and overall rates tend to be higher, making it more expensive. For example, if the company is paying a 6% interest rate on its Debt, and the market value of its Debt is close to its face value, then the Cost of Debt might be around 6%. “Capital” means “a source of funds.” So, if a company borrows money in the form of Debt to fund its operations, that Debt is a form of capital. Also, you should not add back the Operating Lease Depreciation or Amortization because in this case, it represents part of an actual cash expense. GAAP aren’t too bad because U.S. companies still record Rent as a simple operating expense on their Income Statements.

How To Calculate?

Most companies don’t assume that they’ll stop operations after a few years. They expect business to continue forever or at least for a very long time. Terminal value is an attempt to anticipate a company’s future value and apply it to present prices through discounting. Moving onto the other calculation method, we’ll now walk through the exit multiple approach. Next, the Year 5 FCF of $36mm is going to be multiplied by the 2.5% growth rate to arrive at $37mm for the FCF value in the next year, which will then be inserted into the formula for the calculation.

The Big Idea Behind a DCF Model

Yarilet Perez is an experienced multimedia journalist and fact-checker with a Master of Science in Journalism. She has worked in multiple cities covering breaking news, politics, education, and more. Her expertise is in personal finance and investing, and real estate.

DCF Models: Further Learning

This may be useful for valuing companies with a long period of competitive advantage, but where you are unwilling to forecast explicitly for that long. The example of a pharmaceutical company used earlier works well here. They are likely to earn good returns while their patent is in force, and their patent may be a very long one. However, you may be unwilling to make explicit forecasts that far out.

Using the MadDonald case again, the $1000 cash outflow for buying the refrigerator is not counted as expense in the year in which it was paid because the $1000 was capitalized as a fixed asset on the balance sheet. Thus we need to deduct cash paid for these “investing activities” when calculating the cash flow for the year. Capital expenditure should also be projected when you prepare a forecast of the business (In our example it is provided ). The terminal year assumes that a business will continue to generate cash flows at a constant stable rate forever. That is why we stress the importance of the business having matured and stabilized during the projection period. Then, you need to tweak the assumptions a bit to make sure the implied growth rates and multiples make sense.

Given the importance of this concept in DCF, we will explain a bit more what is FCFF and FCFE and how do they differ from each other. It’s important to note that determining the appropriate exit multiple and selecting the right terminal year metric require careful consideration and analysis. Sensitivity dcf perpetuity formula analysis and consideration of industry and market trends are also important to ensure the accuracy of the DCF valuation. This can be assumed based on Capital Asset Pricing Model (CAPM) or any other model or could just be the implicit return rate of the market or as investors require.

There are two principal methods used for calculating terminal values. The perpetuity growth model assumes that the growth rate of free cash flows in the final year of the initial forecast period will continue indefinitely into the future. Terminal Value is the value of the business that derives from Cash flows generated after the year-by-year projection period. It is determined as a function of the Cash flows generated in the final projection period, plus an assumed permanent growth rate for those cash flows, plus an assumed discount rate (or exit multiple). More is discussed on calculating Terminal Value later in this chapter.

Surprisingly, this is actually the most straightforward part in the DCF computation. Given net profit has already deducted finance cost, to compute the FCFF, we need to add back the finance cost as illustrated below. Please note that we need to multiply the finance cost by (1 – tax rate) to account for the tax shield from the finance cost. In our example, the projection period is from FY2019 to FY2023, with 2023 being the terminal year.

If your implied values do not match your assumed values when you perform these checks, there is an error. It’s a best practice to list out your key variables at the top of the file. This allows you to easily keep track of them, and it makes your assumptions explicit to anyone else who might open up the file. The DCF is the most subjective form of valuation – it is subject to the most judgment and potential for manipulation. When we compare it to other valuation methodologies, it has the most unknown variables. Its projections can be tweaked to provide different results for various what-if scenarios.